Luxury Mergers and Acquisitions in 2023: Breathing Some Fresh Air into the Space

“Mergers are like Marriage. They are the Bringing Together of Two Individuals.” – Simon Sinek

If mergers are like marriage, then this summer, the wedding bells have been ringing loudly in the luxury space with a flurry of activity in mergers and acquisitions (M&A). We have also witnessed several investments, capital raises, and an IPO (Initial Public Offering) with Birkenstock listing on the NYSE (New York Stock Exchange) last week. In addition, Puig, owners of venerable niche brands like Carolina Herrera and Paco Rabanne, have just announced their plan to go public. This comes amid an increasingly muted prognosis for luxury and premium brands and much uncertainty and pullback in some formerly crucial growth areas like the US and China. And yet, precisely because of this, we have witnessed a breath of fresh air in the luxury M&A space with some large-scale and, frankly, surprising transactions. There is a noticeable trend towards consolidation, ushered in in 2021 by the LVMH/Tiffany acquisition.

With global M&A activity down about 44% in the first five months of 2023, according to Bain, the luxury industry is no exception to the M&A slowdown. Still, it has recently shown signs of re-ignited M&A activity. However, this activity is characterized and driven by factors very specific to the industry and with varied implications.

What is the strategic context for M&A in luxury at the moment?

Broadly speaking, the strategic motives for M&A activity can include a) brand portfolio expansion, b) market dominance, c) synergies (mainly cost-related), d) creative collaboration, e) global expansion, f) preservation of heritage and g) access to innovation and technology.

Currently, aside from the usual synergies and scale, the two key concepts around which these transactions appear to revolve are control and distribution. This should come as no surprise. Enhanced cost control and more efficient distribution and sales channels can improve margins and growth, in turn ensuring a brand’s staying power, especially in uncertain economic times.

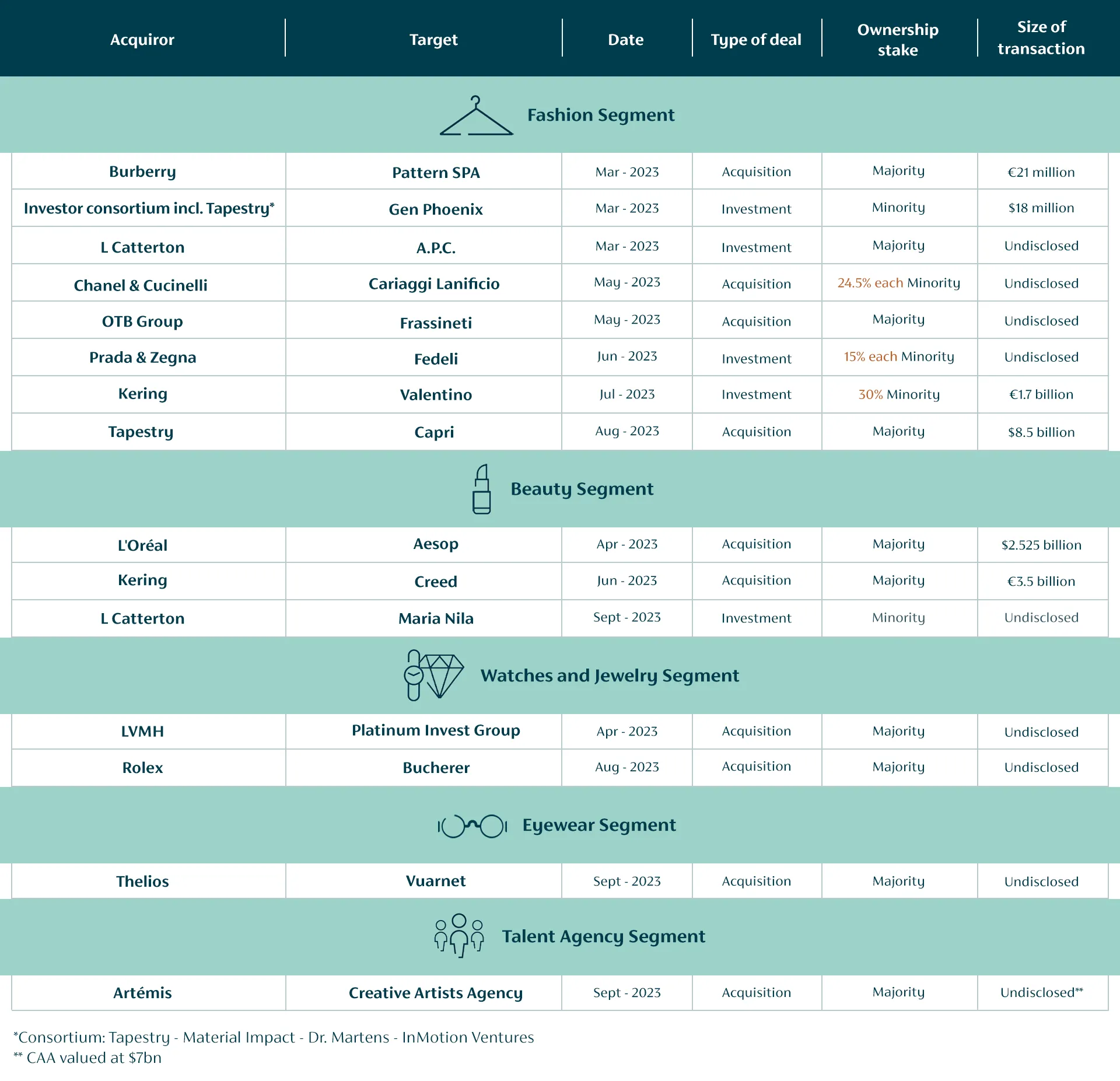

Across the spectrum of M&A activity, we are seeing luxury juggernauts gobbling up their suppliers and distributors in a strategic move at vertical integration. Examples include Prada’s and Zegna’s joint investment in Luigi Fedeli, a knitwear manufacturer and Chanel’s and Cucinelli’s investment in Italian wool and cashmere manufacturer Cariaggi Lanificio.

Others are acquiring “sideways” through horizontal integration, with the aim being diversification or market access. Right now, this is happening in rather surprising, inspirational and truly forward-looking ways, as in the case of the Kering/Creative Artist Agency acquisition.

The general rule of M&A is that when valuations are poor, deals become less attractive to sellers or targets and M&A activity tends to shrivel. However, at a time when money is expensive, large luxury and beauty conglomerates have seen their valuations and, thus, their capital base rise to unprecedented levels. At these hefty valuations, these acquirers have large amounts of relatively inexpensive capital to purchase vendors and distributors or other targets. Smaller companies may be facing uncertain times ahead as inflation gathers steam with a potential looming recession. This leads to a confluence of factors, making resistance to attractive price offers difficult and rendering strategic mergers or investments a sensible option.

The large groups also have the capital to invest in smaller founder-based high-growth targets and diversify into industry-aligned but non-traditional segments.

What is happening across the different industry segments?

Beauty and Cosmetics

With resilient profit margins and the possibility of scalability, the beauty sector has many attractive prospects representing interesting acquisition targets for larger groups. Beauty is especially desirable to consumers as it represents a luxury category carrying affordable products. This renders the sector somewhat more recession-proof than others.

Watches and Jewelry

On the other hand, this sector, long a haven of traditional wholesale distribution, appears to be in the initial stages of an industry shake-up, both in terms of the rise of the pre-owned watch segment and an increasing tendency towards Direct-to-Consumer (DTC) operations. The favorable perception of watches and jewelry as investment products with lasting and even increasing value is also a boon for this industry in challenging times. What do these two sectors have in common from a financial point of view? More resilient margins than luxury fashion and accessories and, in theory, more room for growth.

Fashion and Accessories

In the premium or aspirational segments, margins and profits have been under pressure due to consumer pullback. Acquisitions in this segment are driven by a need to create larger, more cost-effective distribution networks, enter new geographic areas to drive growth and build scale to control costs. In the luxury and absolute luxury segments, we have witnessed resilience and continued growth. Here, the name of the game is strategic growth, expansion and diversification.

Getting to the crux of the matter: What are the implications of some of the more prominent landmark deals we have seen for the industry at large?

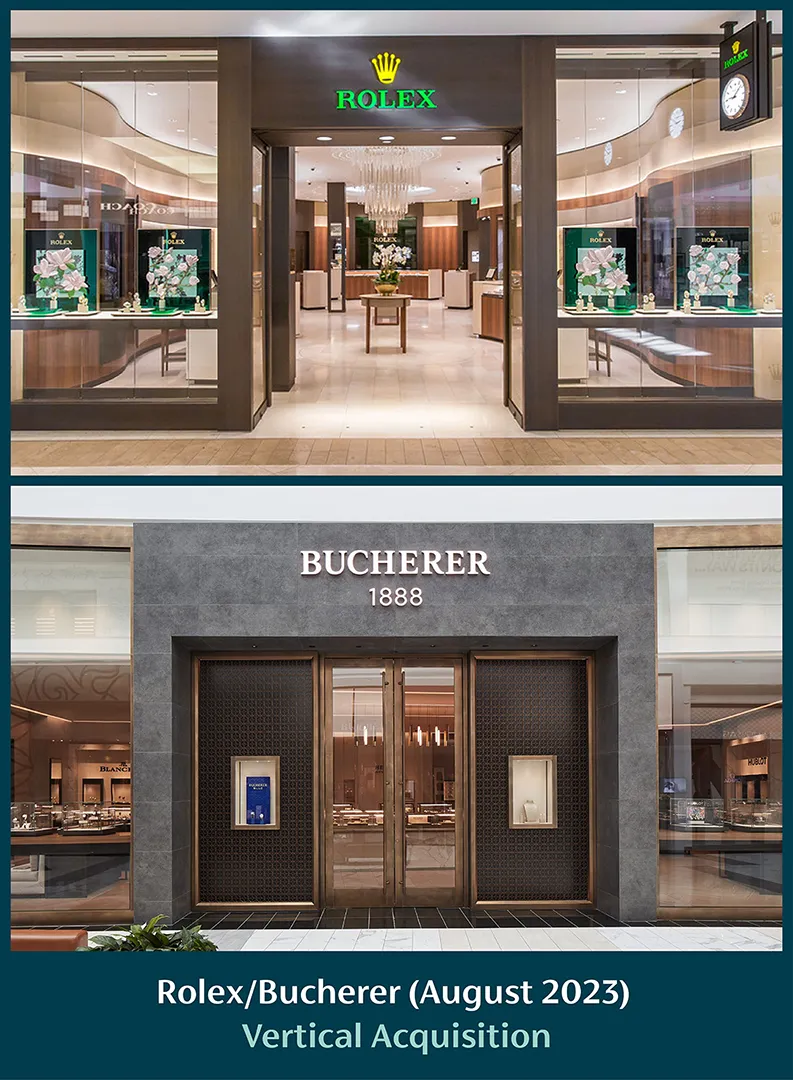

Rolex/Bucherer (August 2023) – Vertical Acquisition:

In a strategic move to establish a significant presence in DTC sales, Rolex announced its acquisition of luxury retailer and long-time partner Bucherer, which owns 100 stores worldwide. The company will continue to operate independently under its name and sell other watch brands. This vertical acquisition allows Rolex to sell its watches through owned retail, providing it with optimal control over the distribution of its new and pre-owned watches and also an enhanced ability to control its branding, marketing, and customer experience in stores. It is an unprecedented move in the W&J industry and is part of a dynamic reshaping of the industry.

CXG View on Motive: Cost Synergies and Market Dominance

This vertically integrated deal broadens sales channels, effectively allowing Rolex to become DTC, enabling enhanced control over branding and marketing, and allowing the brand to create an improved customer and retail experience and better customer engagement and loyalty. It allows for margin improvement and scalability while giving Rolex unprecedented access to its competitor brands’ sales and CRM information.

Tapestry/Capri (August 2023) – Horizontal Acquisition:

Tapestry acquired Capri, the parent company of Michael Kors, Versace and Jimmy Choo, for $8.5 billion to create a new powerful global luxury house. This merger will strengthen the two companies, which took a big hit during Covid from the disruptions in China, impacting both manufacturing capabilities and consumer spending. Both companies, especially Tapestry, are also exposed to the squeeze on aspirational luxury spending in the US amid soaring inflation.

CXG View on Motive: Cost Synergies, Global Expansion and Market Dominance

This deal is primarily driven by scalability and distribution, but is also about entry into “true luxury.” The purchase of Capri, a group of luxury brands, is an effective way for Tapestry, which holds a collection of more premium brands, to enter the world of absolute luxury without having to scale the business organically. Combining these two powerhouses will allow their brands’ international expansion to take place with more resources, capital, and a wider network. Capri brands will also be able to tap into Tapestry’s quite developed omnichannel eco-system, particularly in China.

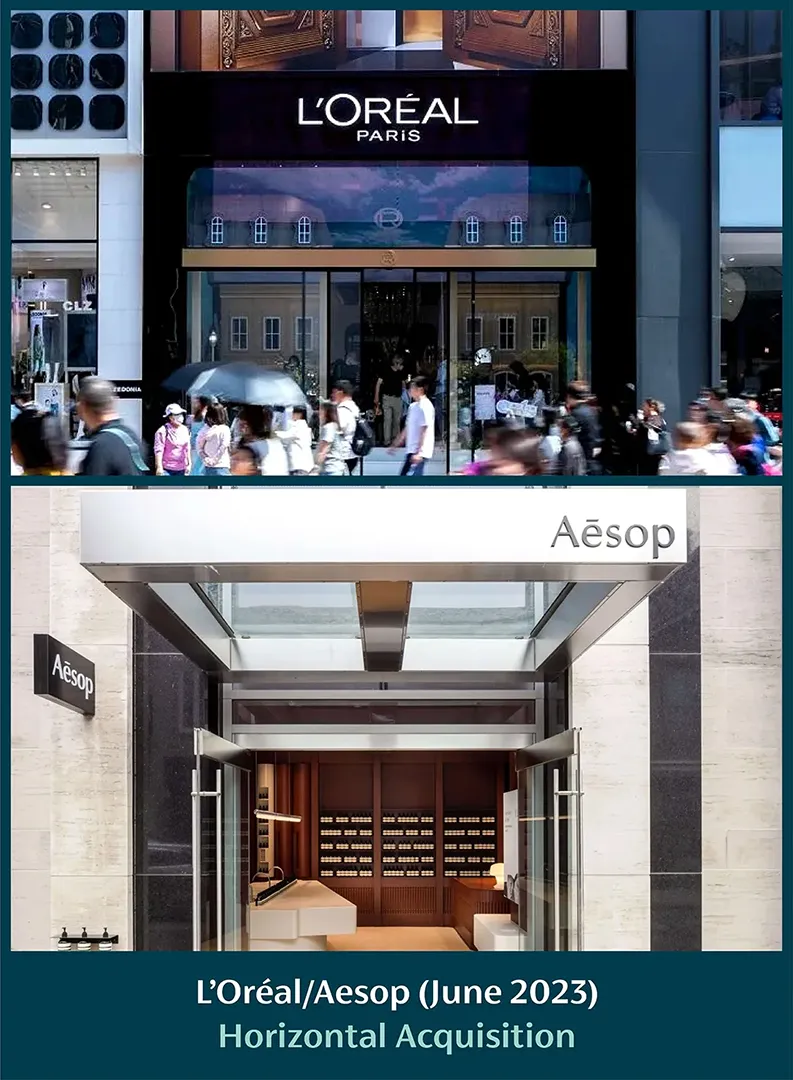

L’Oréal/Aesop (June 2023) – Horizontal Acquisition:

L’Oréal acquired Aesop, the upscale Australian clean beauty cosmetics brand, in a deal valued at $2.525 billion. This is the largest-ever acquisition for L’Oréal. L’Oréal will help accelerate Aesop’s growth potential by focusing on travel retail and global expansion, mainly in China. The brand resonates with many new consumer trends, especially sustainability. Aesop is currently being sold in 400 retail outlets and has established partnerships with luxury hotels and beauty centers.

CXG View on Motive: Market Dominance, Access to Sustainability/ Innovation/ Technology, and Brand Portfolio Expansion

One of the main drivers behind this acquisition is the ability to automatically enter the “clean” or organic beauty space without having to scale a business internally. Aesop’s strong affiliation with the hospitality space and beauty centers is a further advantage in terms of distribution. Combined with the prowess of the L’Oréal brand, which includes its beauty science and beauty tech innovation, as well as its global reach and economies of scale, Aesop can be built into a worldwide powerhouse brand while giving L’Oréal the ability to tap into and learn about the clean beauty business for future expansion.

Kering/Valentino (July 2023) – Horizontal Acquisition:

Kering acquired a 30% stake in Valentino from Qatari investment fund Mayhoola for €1.7 billion. The deal includes an option to buy the remaining stake over the next five years. Mayhoola also owns the French brand Balmain and the Italian brand Pal Zileri.

CXG View on Motive: Brand Portfolio Expansion, Global Expansion and Market Dominance

Since Kering’s Gucci has hit some roadblocks recently, the Valentino brand could give Kering a necessary sales boost and balance out the slowdown at Gucci while the latter repositions itself with a new designer and leadership. This acquisition makes a lot of strategic sense and reflects a head-to-head race regarding market dominance between the large luxury groups. Unlike Gucci, which has already almost tapped out its global and product expansion, Valentino still had significant room for growth in terms of worldwide retail expansion, omnichannel growth and product assortment. Its Web3 strategy is also interesting and aligns with the efforts Gucci has been making in this space already.

Kering/Creative Artist Agency (September 2023) – Mixed Horizontal/Congeneric Acquisition (i.e., in complementary segments):

Artémis, the Pinault family’s investment company, has agreed to buy private equity firm TPG’s majority stake in renowned Hollywood agency Creative Artists Agency (CAA) in a mega-deal reported to be worth $7 billion. Artémis, with assets under management of around $40 billion, controls Gucci and Saint Laurent and auction house Christie’s. CAA, founded in 1975, is a talent agency representing some of the top stars in sports and entertainment globally. Last year, CAA acquired ICM Partners, another major creative talent agency. CAA has also expanded beyond film and music to represent many professional sports stars, including big names in soccer, football and other sports.

CXG View on Motive: Creative Collaboration, Brand Portfolio Expansion and Diversification

While CAA will be managed independently, the connection between fashion and entertainment is at an all-time high with the appointment of Pharrell Williams at Louis Vuitton and many ambassadorships between luxury houses and music, film and sports stars. This can help Kering/Artemis go head-to-head in their race against competitors to secure talent that will drive brand awareness and enhance reach.

While the talent management business is technically unrelated to luxury and fashion, the ties between film, music and sports and luxury and fashion have never been stronger. This transaction creates diversified and, at the same time, highly aligned and interconnected revenue streams for Artemis and, by extension, for Kering.

Why do we care and what could these deals imply for customer engagement, loyalty and quality of experience?

Luxury M&A can lead to improvements in overall customer experience both offline and online. This is unlocked when synergies lead to savings that are then redirected and applied to improve customer experience and elevate the brand. Enhanced customer service, better branding and marketing, personalized shopping experiences and omnichannel integration, as well as better access to technological innovation, can all be consequences of successful acquisitions and integrations of brand portfolios.

Especially in the case of vertical integration of vendors, control of the supply chain can mean enhanced product and service quality, as well as more traceability when it comes to provenance and sustainability. Vertical integration of distributors, on the other hand, allows for tighter control over sales and distribution, more detailed customer insights and the ability to build closer connections with customers. These factors can make a big difference in the overall customer experience and allow brands added differentiation.

However, the challenging aspect of mergers and acquisitions can often be the preservation of the uniqueness of a brand’s DNA, heritage, culture and messaging. Sometimes, integration can be costly and diverts attention and funds away from the brands’ clients instead of being an opportunity to create enhanced customer experiences and increased loyalty and engagement.