Less Is More: Quiet Luxury Has Not Lost Its Luster

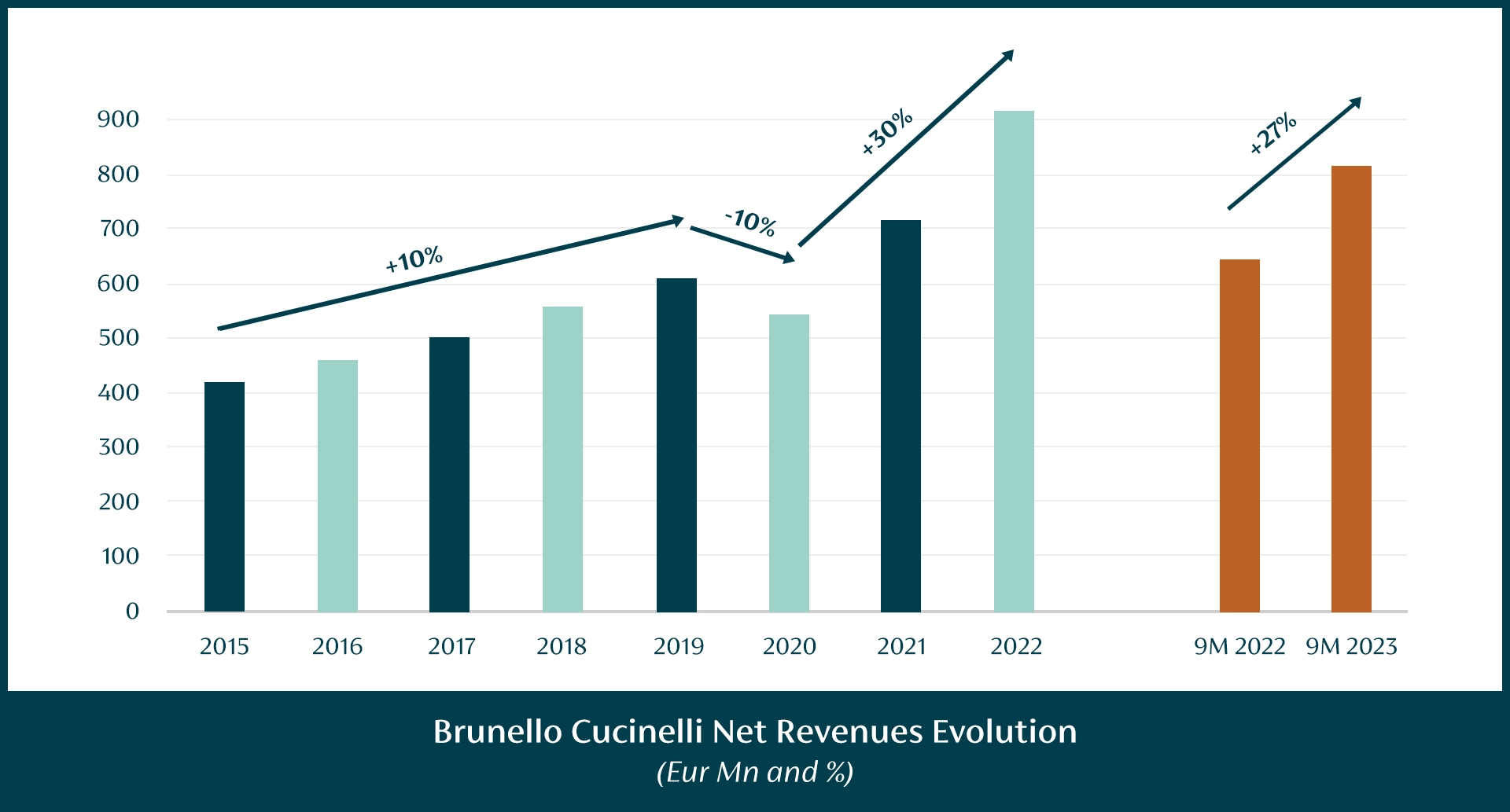

Brunello Cucinelli’s recent 9M 2023 results flew in the face of the general trend in luxury earnings season and what we have come to expect at this point, namely news of significant slowdowns in growth. While all the talk of quiet luxury has been fascinating as another qualitative data point about trends, actual proof has come from financial results. Cucinelli posted a 27.5% increase in revenue, with China contributing with an astounding 49.7% increase, while the US showed very healthy growth at 21.7%.

One cannot help but be impressed by the positive results amid a worrying economic environment and geopolitical uncertainty. It is also impossible not to infer a correlation between the stupendous growth of the brand, the role of the ultra-wealthy, and the company’s ethos of understatement, quiet luxury, and soft elegance. Cucinelli, while still a relative “David” among the “Goliaths” of luxury, is the epitome of quiet luxury and is recognized for its top-notch quality materials and execution.

As economic uncertainty and higher inflation are gnawing away at the spending power of aspirational customers, the truly wealthy remain insulated from these woes. They continue to spend, but their splurges are motivated by top quality, casual elegance, understatement and investment value, across apparel, leather goods, or jewelry. The continued demand from wealthy customers at the top echelon of luxury brands and the recent Q3 earnings resilience of several brands, including Cucinelli, Zegna and Hermès is quantitative confirmation of the strength of understated luxury and somewhat of a bright spot for luxury.

It is, therefore, not surprising that Gucci’s hotly anticipated turnaround collection “Ancora” eschews flashiness and opulence in favor of minimalism and understatement.

The above leads us to draw several conclusions:

1. Quiet Elegance Trumps Flash

Luxury customers are looking for the highest levels of craftsmanship, quality, and rarity and are still willing to pay top dollar for this level of luxury. This is especially true of the very wealthy but is becoming a general trend in luxury. Not only are customers expecting this level of quality in the products, but also in the service and experiential components of the interactions. The key words are “quiet elegance”, eschewing any signs of flash or opulence.

2. High-end Positioning as Crisis “Immunity”

With Cucinelli charging an average of $10,000 for a cashmere coat, this is luxury in the absolute realm and not accessible to the “regular” luxury customer. Brands catering to a very high-net-worth clientele as their core focus with assortments that have no entry-level products have the pick of the market share right now.

3. Chinese Customers are still into Luxury – the Quiet Kind

Despite a lackluster performance in China, Chinese ultra-wealthy luxury customers seem to have developed an affinity for understated luxury, with the logo craze relegated to history. China’s own luxury brands are embracing a similar aesthetic, Icicle and Erdos being perfect examples of the future of Chinese homegrown luxury brands. The results for Hermès and especially Cucinelli in China are solid confirmations that the luxury customer is well and alive but is shopping with intentionality centered around ultra-luxe and understatement.

4. The US Shows Resilience in Ultra-Luxe Brands that Represent Investment Value

In the US, many luxury brands are witnessing a pullback in luxury consumption, with several of them barely posting single-digit growth. This development became apparent at the start of 2023 but has really cemented itself in Q3. Insulated from this trend, however, are luxury brands like Hermès and Cucinelli, which have grown at high double-digits in Q3.

5. There is Room for Brands Positioned to Upscale: Spotlight on Zegna

Zegna posted healthy YoY growth in Q3 at 21% (with a notable 44% YoY increase in North America), confirming the strength of consumption based on intrinsic value and the continued resilience and buying power of High Net Worth Individuals (HWNI). When a brand is well positioned structurally and has the financial wherewithal, as well as the brand equity, to engage with a higher-spending customer, it can successfully upscale and tap into this market.

What is next?

Quiet luxury is not just a temporary shift in tastes, but seems to be a future mainstay. The challenge for brands with a mixed customer base is to foster their engagement with HNWI (for example, through more understated, elevated collections) while simultaneously continuing to keep the aspirational customers in the mix. The formula for such a strategy involves both art and science. And importantly, it is not solely the product, but also the customer experience that forms part of this elevated package. Immersive signature experiences, excellent service, and on-point messaging are still key differentiators.